The Moneyshot: Day 22

Today is the end of my first month of rigorous budgeting, and I can tell you this: I suck at budgeting.

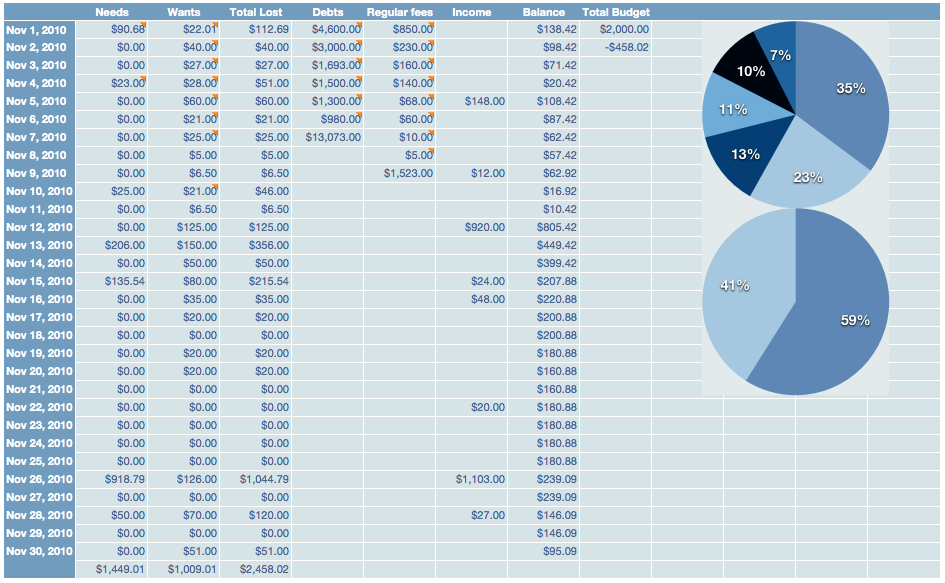

The upside of all this drama is that in failing, I will succeed. Take a gander at November’s wrapup.

Almost $460 over budget. That means that I could have used that money’“plus the money I had supposedly earmarked for paying down debts’“and gotten rid of nearly $1,000 of credit card debt. That’s a powerful lesson for me, and hopefully for anyone who’s followed the series thus far. You can see how easy it is to spend gobs of money without paying attention, and I admit more than most that I was not paying attention.

Almost $460 over budget. That means that I could have used that money’“plus the money I had supposedly earmarked for paying down debts’“and gotten rid of nearly $1,000 of credit card debt. That’s a powerful lesson for me, and hopefully for anyone who’s followed the series thus far. You can see how easy it is to spend gobs of money without paying attention, and I admit more than most that I was not paying attention.

Going forward, my posts are going to be monthly as it makes less sense for me to talk about this every week. Just like therapy, you have an intensive series of sessions at the beginning and scale back as time goes on. I hope you’ll follow me as I pay my debt off, and hopefully find along the way that you make a lot of the same mistakes that I do.

A few observations: yes, my credit card debt swung up slightly. I used my cards (re-maxed them out) because I was cash poor. My goal next month? Don’t use them at all. On top of that, stop being freaking cash poor. That means I may have to skip a month of paying down debt yet again, but if it means I have cash to float on, so be it. Liz Pulliam Weston advocates not doing that as it makes less financial sense in the long run, but I can’t keep using my credit cards. I have to have cash as many places I go to don’t accept credit. Or perhaps that’s the lesson here, to cut myself off? Only this month will tell what I end up doing.

Areas of opportunity: my food budget is low, but I can send it far lower. I’m a big meat and potatoes guy, and if I start cooking for myself, I can get by on $20 a week. That would halve my food budget, and I’d have that extra for Christmas presents. For the sixth year running, my family has stuck to its policy of no-gift Christmas, so I’m just going with token gift cards for the kids. I may renege on that and bake for them instead. I have yet to decide, but I have to make up my mind quickly. That’d bring in $80, by the way.

I’ve also scaled back my mental health visits, as I have been pretty darn happy despite all this. I’m going to my therapist now twice a month instead of every week, so that’s an extra $30.

Although I advocate smartphones, I’ve found that I don’t actually use the phone portion at all. Looking into pay-as-you-go plans, I can ditch my phone and pay $25 a month to have unlimited texting and Skype for just about everything I do call-wise. I’d have to go back to a flip phone (ugh) but it might be worth it, since I’d be able to get a PDA to handle all my other stuff. That would mean a savings of $40 a month from my cell.

That means that right off the bat, I’ve freed up an extra $110 from my budget with a total $150 possible if I can ditch my smartphone this month. I’m probably going to sit back and wait to see how the tablet computer market goes next year first, but by April I plan to be smartphone-free since I never use the data, never use the voice, and only use the texts. It is not worth the cash to text someone for $70 a month.

On the tricky situation of porn, about which you all were extremely supportive and sweet bee tee dubs, I spoke to my therapist about it and he said that especially creative people suffer with the need to create. Without that need fulfilled, they will look for other sources, which is apparently what I’ve been doing. As a result, I have planned out my next six months chock full of new projects, endeavors, and creative pursuits to keep me off the paid porn sites (and free ones, for that matter) and doing stuff with my life that I’d rather do. I don’t know if anyone else out there has struggled with this like I have, but I hope that sheds a bit of light on it for everyone.

Let me know if you have any feedback. Next week: financial makeover for a lucky guinea pig!

Clint,

Fun series! It does take a lot of guts to put all your finances out there for the internet to see. Kudos to you!

I think you’d have more success if you tried to gradually change your spending. There’s no way anyone can sustain a permanent drop in spending in some area. I think it’s much more sustainable to lower it by some amount every month until you hit your target. Like if you spend $500 a month on something (eating out, porn, etc.) then the next month aim for $480 or $450. Keep dropping it a little bit per month from there. That way you are still consuming things you love, but not noticing the decrease that much. You’ll get used to it over time. I think you’ll be successful if you plan for it.

And I’m not sure if you should chop out all of your discretionary spending. Sure, saving $30 a month on therapists would be nice, but how will that affect your mood and all? “Investing†$30 extra per month on the therapist might give you a good “return†in the form of mental clarity or ideas that will give you energy to put into creative, income-producing side projects. For reference, I cut back on my food budget but now I’m REALLY feeling it because my energy levels are way down.

But keep up the good work. I love reading this stuff. Budgeting is hard, so don’t let it get you down too much.

Clint, you’re making some good changes. Every little bit will make a big difference in the end. Can’t wait to hear your next update.

Good luck Clint! I’m rooting for you and can’t wait to read the next update.